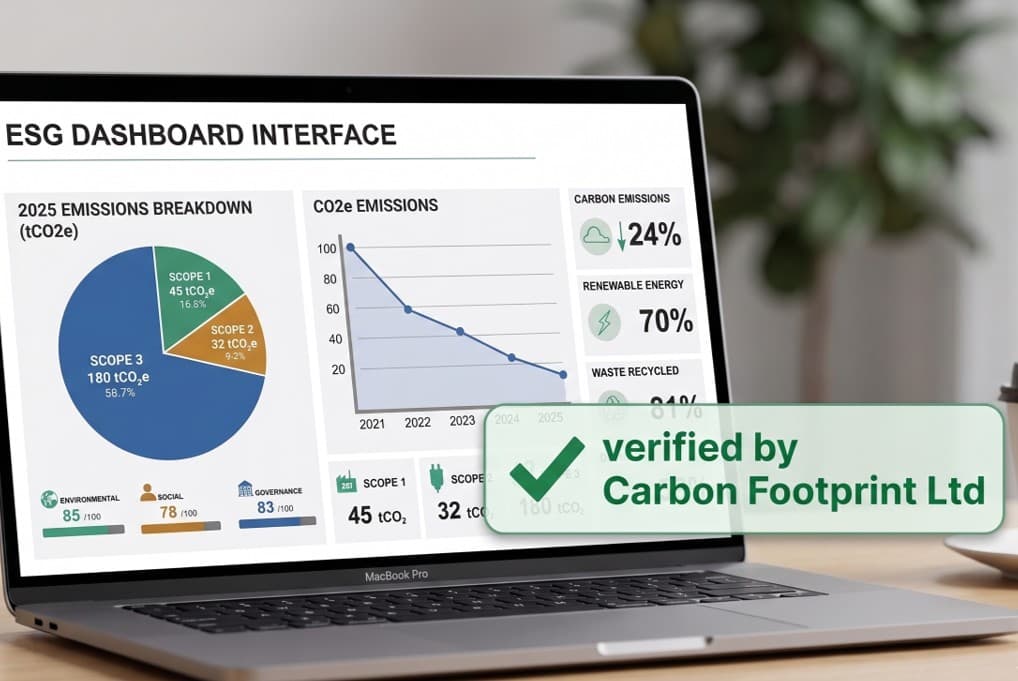

Compliance · Streamlined Energy & Carbon Reporting

SECR compliance, powered by Sustrax

Accurate energy and carbon reporting is now a legal requirement for qualifying UK businesses — and it shouldn't mean a year-end scramble. We combine world-class consultancy with powerful software for audit-ready SECR reporting.